PVH Looking Towards China To Power Growth

noel bennett/iStock Editorial via Getty Images

PVH Corp. (NYSE:PVH) looks appropriately valued when weighing its current valuation versus its long-term opportunities and the potential for economic weakness later this year.

Mục lục

Company Profile

PVH is a global apparel company that owns and licenses a number of well-known brands. Its owned brands include Tommy Hilfiger, Calvin Klein, Warner’s, Olga, and True&Co. The company sold several brands, including Van Heusen, IZOD, ARROW, and Geoffrey Beene, to Authentic Brands Group in 2021.

Calvin Klein and Tommy Hilfiger account for over 90% of PVH’s revenue, with Tommy the slightly larger brand. It sells the two brands through two primary distribution channels: wholesale and retail. Through the wholesale channel, the company sells its apparel through department and specialty stores and their related websites. In North America, it also sells through warehouse clubs and off-price retailers.

The company also sells both brands direct to consumer through its own retail stores and websites. Its North American stores are primarily in premium outlets, while in Europe, Asia and, in the case of Calvin Klein, Brazil, the company operates both full-price and outlet stores.

The company also licenses its brand to third parties. For example, it licenses the Calvin Klein brand to Coty (COTY), which I wrote up here, for fragrances. While it licenses the Tommy Hilfiger brand to Movado (MOV) for watches and jewelry.

Each PVH brand has in-house design teams that are responsible for creating new designs and products. They then work with the brand’s merchandising team to analyze market trends, sales, and consumer preferences. Products are then produced by independent manufacturers, mostly located in Asia.

Opportunities

China is perhaps PVH’s biggest growth opportunity. The country is only about 6% of PVH’s revenue, but it sees the potential to grow the business 5x the level it was at in 2019 by 2025.

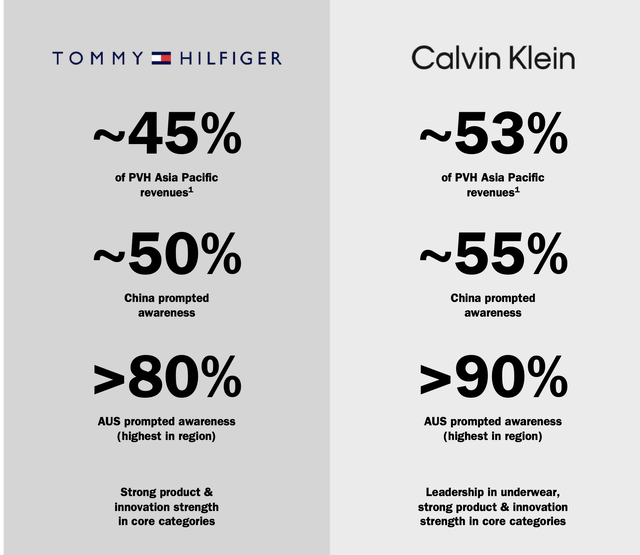

China is a very luxury-brand driven market, and thus most sales are at full price. The brand awareness for Calvin Klein and Tommy Hilfiger in China remain relatively low around 50%, compared to well over 80% in places like Europe and Australia. As a result, the company has struck partnerships with leading Chinese digital firms such as JD.com, Tmall, and Douyin. Note that Douyin is similar to TikTok and owned by the same company ByteDance.

Company Presentation

Covid-related lock-downs obviously stalled growth in the country, but a Chinese re-opening should help power growth. The company, meanwhile, is seeing momentum in other parts of Asia as well, and expects to reach a $1 billion in sales in the region by 2025. In Q3, the region saw 30% growth ex-China, despite a 15% currency headwind, demonstrating the momentum the Calvin Klein and Tommy brands have in Asia.

In North America, the company has become too exposed to the value channel, de-valuing its core brands somewhat. Reducing its exposure to the value channel and repositioning its brands to a higher-end status should help its image and lead to better sales and margins. This is a common problem that can show up for brands. Kors, owned by Capri (CPRI), and Ralph Lauren (RL) have had to execute similar brand repositioning strategies. The company believes this transition will take a few years to complete.

Shifting more to the direct-to-consumer (DTC) channel is another opportunity for PVH. In 2021, the mix was about 65% wholesale and 35% DTC. Digital is a huge growth driver across regions and can be margin accretive. A lot of PVH’s investments will go towards the digital channel to improve the customer experience and drive growth.

Risks

As with most apparel companies, PVH’s sales can be sensitive to economic conditions. About 60% of its sales come from international markets, so how the European and Asian economies are doing can impact its results. A recession is generally not great for mid-tiered apparel companies.

PVH also still has a lot of wholesale exposure to places like department stores. The struggles of department stores are well documented, as malls in U.S. and Europe have fallen out of favor with shoppers. Pre-pandemic, about 12% of its sales were from department stores, although the make-up of the company was bit different back then.

As noted above, the company has gotten too much into the off-price channel. While fixable, this is an issue and it can become disruptive. A consumer pullback or recession would also make this issue more difficult to fix quickly.

A company like PVH also always faces fashion risk. Consumers can be fickle, and if Calvin Klein or Tommy miss trends or the lines become stale, it can hurt sales. Brands can go in and out of fashion, and both Calvin Klein and Tommy have been in and out of fashion in the past.

Inflation is another risk, as the cost of raw materials, labor, and freight have all been of the rise. The combination of higher input costs and reduced consumer earnings power can be detrimental to apparel companies.

Valuation

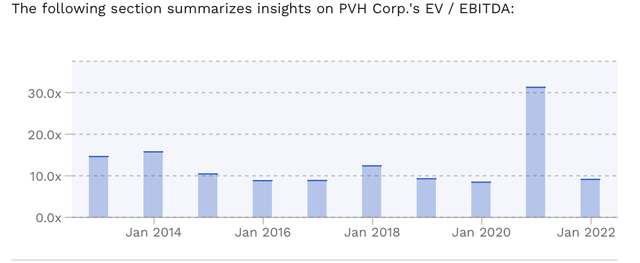

PVH currently trades around 7.2x the FY 2024 (ending January) consensus EBITDA of $1.11 billion and 6.5x the FY25 consensus of $1.23 billion. Historically, the stock has often settled into a 8-10x trailing EV/EBITDA multiple.

PVH EV/EBITDA Historic Multiples (FinBox)

It trades at a forward PE of 8.8x the FY24 consensus of $8.97.

PVH is projected to grow revenue 3% in FY24 to $9.2 billion and nearly 4% in FY25 to $9.5 billion.

RL by comparison trades at an EV/EBITDA multiple of 8.3x FY24 EBITDA (ending March) and a forward PE of 12.9x. RL is projected to have mid-teens revenue growth. CPRI, meanwhile, trades at 7.8x FY24 EBITDA (ending March) and a PE of 7.3x. It’s projected to grow revenue mid-single digits.

Conclusion

PVH’s stock has rallied nicely off its lows from last fall, but the stock hasn’t really done much over the past decade. It has some opportunities to grow in Asia and continue to increase digital penetration, but it’s still expected to be a slog to grow the business. Meanwhile, Calvin Klein and Tommy aren’t exactly known to be go-to brands among teens and young adults.

PVH Price Chart (FinBox)

With the stock trading slightly below its historical multiple, but facing possible economic headwinds, I think the stock looks appropriately valued and that there are better opportunities out there.